Reducing costs and accurate charging of IT Services

The relationship between the supplier of IT services to a major UK Utility and its client was becoming more and more fraught. IT managers' time was increasingly dominated by negotiations over budgets for IT staff and estimates of time for additional work. Both parties approached negotiations believing the other to be at fault. The IT managers suspected their opposite numbers were out to build reputations as tough negotiators by paring IT budgets to the bone regardless of the effects on service quality. Client managers, on the other hand, suspected their IT counterparts were retaining too many staff, all of whom had to be charged to the client by fair means or foul.

An exhausting, frustrating and time consuming process resulted that left all parties dissatisfied with the end result. With the information to hand no-one really knew whether the resources agreed would meet the likely demand for IT services in the future and whether they would represent good value for money. However, within 4 months both sides had a clear understanding of the costs of the activities that made up each of the key services. Negotiations were positive, brief, and focused upon predictions for the root causes of activities. Client managers were able to finely tune their spend by minimising the root causes within their control. IT managers were able to help them to minimise their spend further by reducing the costs of activities over time. As a result:

- Overall spend declined for the first time since IT was outsourced - a saving of £1m over three years without any drop in service quality

- Far less time was spent on budgeting and a stronger partnership between client and provider developed allowing them to deliver new services to the end customer more quickly.

Budgeting - not the route to consensus

The IT supplier provided new development and operations plus support to existing systems. All services were charged to the client at cost, with a percentage margin placed on top.

The resources needed for new developments were agreed relatively easily. Sophisticated project planning tools gave credibility to the numbers reached. Because most new applications were intended to generate additional revenue and development resources were capitalised rather than met out of revenue budgets, a favourable financial calculation usually resulted. Project budgets could therefore be generous.

The same did not apply to operations and support for existing systems. Each year both parties had to agree the budget for services. Any unforeseen work had to be negotiated separately as the need arose. Because much of this work did not produce such a favourable financial outcome, negotiations were often fraught with difficulty. The critical problem facing both sides was that value judgements for operations and support were difficult to evaluate - even though failure to perform certain tasks could put the client's business at risk. Costs were the only parameter that managers could debate.

The whole process of negotiation was made more difficult by the pressures placed on both parties. Client managers were required to halt what had been, in recent years, a steady rise in IT operations & support spending. The belief that further increases would deliver little tangible benefit was widespread. Increases, they argued, would simply help shore up an inefficient, over-staffed organisation rather than deliver much needed improvements in service.

IT managers, on the other hand, were under pressure to keep the contract with their client intact at all costs. Large, long term contracts were hard to find. It was vital that the relationship improved. IT resources were already stretched to breaking point. Problems arising from an upgrade to a new desktop standard as well as the rollout of new mainframe applications meant that some people were already working as much as 70 hours a week.

Nevertheless, the financial arguments supporting the need for more resources were weak. They were unable to answer the client's most fundamental questions: what was it essential to spend; how could the size of the increase be justified; what was desirable but not essential; where could savings be made? Without a better understanding of the costs involved, both sides remained unable to reconcile their different positions. A breakdown in the relationship was just around the corner.

The financial reporting systems originated in the days when IT was simply an in-house cost centre. They provided accurate costs of all the people within operations and support, and, through a project costing system, the cost of any separately specified piece of work. However, they gave no clues about the costs of services to the client, the costs of the component tasks, and the impact upon costs of the many factors that influenced the level and quality of services.

The true drivers of cost

Over the next 3 months, as part of an Activity Based Costing (ABC) implementation, each of the key services was defined and costed. As information began to flow out of the work, the relationship began to improve.

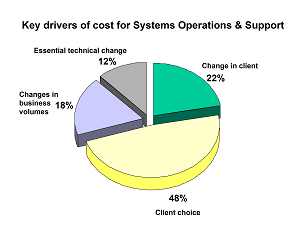

For example, the data quickly revealed that 70 per cent of the total costs of operations and support were

driven by client requests (see Figure, right).

Until then, the client had been haggling over the cost of a help desk technician here or a mainframe analyst there.

They now began to realise the degree to which their own behaviour had a dramatic effect on costs.

Attention on both sides now switched to the nature of the client's requests.

For example, the data quickly revealed that 70 per cent of the total costs of operations and support were

driven by client requests (see Figure, right).

Until then, the client had been haggling over the cost of a help desk technician here or a mainframe analyst there.

They now began to realise the degree to which their own behaviour had a dramatic effect on costs.

Attention on both sides now switched to the nature of the client's requests.

The client changed some part of its organisation several times per year each resulting in the migration of people and their equipment around the business. In one case an entire office relocated to a new site. Six months later, due to changes in another part of the business, they relocated back to their original office.

The client initiated over 200 investigations into new technology and methods each year. However, 55% led nowhere. They were commissioned by different people within the client. Several ended up investigating the same subject.

In an attempt to constrain costs, the client had insisted on allowing only incremental increases in network capacity, typically when someone complained about the poor performance of their machines. In consequence, many small changes occurred rather than a few large ones.

Fact began to replace emotion as the true cost drivers of operations and support were understood by both sides.

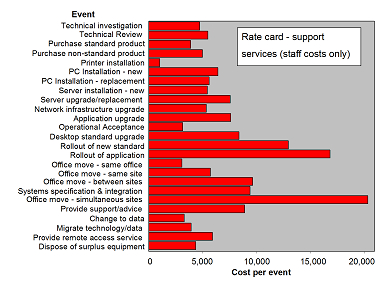

One outcome was the introduction of a rate card for services (see Figure, right).

Fact began to replace emotion as the true cost drivers of operations and support were understood by both sides.

One outcome was the introduction of a rate card for services (see Figure, right).

Both parties could now work together on the likelihood of future scenarios.

Whenever an event occurred, accurate predictions of resources were immediately available. New events would still have to be estimated from scratch, but the estimating process was much easier than before, and less contentious.

Negotiations over IT costs were transformed from antagonistic, long winded debates about the need for people, to positive and brief discussions about the need for activities. This gave the client a real feeling of control over IT spending for the first time. The supplier benefited as well. Given stable prices, a reduction in costs would grow the margin made on services.

Growing the margin on services

Opportunities to reduce costs soon followed.

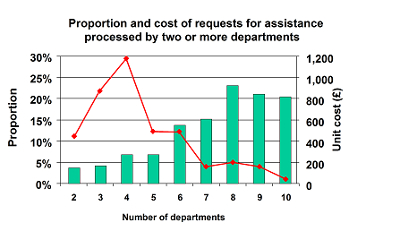

Despite attempts to manage rigorously the handling of user problems, far more people were involved in

fire-fighting than was first thought (see Figure, right).

Opportunities to reduce costs soon followed.

Despite attempts to manage rigorously the handling of user problems, far more people were involved in

fire-fighting than was first thought (see Figure, right).

Over 25% of problems recorded within the help desk database were referred to people within six or more different departments before a successful diagnosis was made. In each case, the cost incurred swelled to many times that of problems diagnosed swiftly.

By improving the user and help desk procedures for first level data collection the proportion of problems diagnosed rose significantly, halving the costs of problem resolution.

Other insights into cost reduction opportunities followed:

- Suppliers for products had always been selected on the basis of price alone. It emerged however that three suppliers in particular had a poor record of successful order fulfilment, and a record of delivering poor quality products. When the full cost was revealed of dealing with the litany of errors, the need to chase delivery and the arguments over payment, all three were dropped.

- The costs of problems arising out of unfamiliarity with new Windows NT client systems accounted for over 25% of the total cost of problem resolution. This dropped to under 10% after traveling road shows were commissioned, at the IT supplier's expense, aimed at addressing the most common user problems.

- At last, with prices made stable through the use of the rate card, the IT supplier could enter into a process of continuous improvement and expect a prize at the end: a growth in the margin made on services.

- Having suffered the agonies of a cumbersome annual budgeting process, the client was able quickly to predict the effect that changes in the market place would have on IT resources. They are now beginning to question whether they need a budget process at all.

The partnership between the two parties has flourished. Both understand each other's goals and recognise that, with the use of sound activity based information, they can work together to achieve them. As a result, the contract for IT services has not only remained intact but will almost certainly be renewed.

Benefits demonstrated by using ABC analysis