Managers-Net

Case Study

Uncovering unprofitable products and customers

A brewery had annual sales of approximately £50 million and was suffering long term decline.

The company had around 1,000 people in the brewery, warehouse and managed estate.

They also had tenanted pubs. Their wholesale wines and spirits division, which accounted

for sales of around £10 million, operated in a highly competitive market.

Although margins overall were shrinking, management suspected that some parts of the

business were performing worse than others. But the gross margins of the different product

groups and customer segments, as reported in the management accounts, and used as their

key performance measure, all looked fine. Managers suspected that gross margins had

become an inadequate measure of profitability, masking hidden costs. The company needed

to understand its net margins - for all its products, for all its customers.

The objectives of the project were to create an ABM model of net product and customer profitability,

train the company's staff in the principles and techniques of ABM and in model-building,

and to draw conclusions from the results.

Results

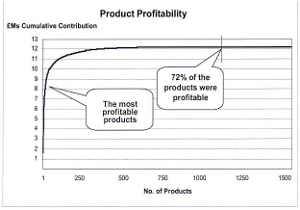

For each product, the contribution to profits

was calculated by subtracting from

its revenue all costs that supported it or that

were driven by it. The results were presented

graphically (as shown right) by sequencing

the products by size of contribution, biggest

on the left, and plotting the cumulative

contribution of them all. Although a number

of products were highly profitable, about

40% of them provided close to zero

contribution - the flat part of the graph.

For each product, the contribution to profits

was calculated by subtracting from

its revenue all costs that supported it or that

were driven by it. The results were presented

graphically (as shown right) by sequencing

the products by size of contribution, biggest

on the left, and plotting the cumulative

contribution of them all. Although a number

of products were highly profitable, about

40% of them provided close to zero

contribution - the flat part of the graph.

The last 28% were marginally losing money.

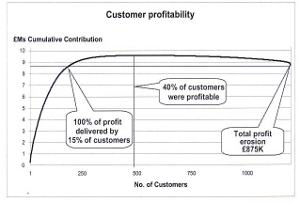

A similar exercise was carried out for each

customer.

A similar exercise was carried out for each

customer.

The result was a shock:

Only around 40% of their customers

were profitable.

The rest were losing

the company £875K.

100% of the profit delivered by only 15% of the customers

For example:

Further analyses showed up other interesting

results, some of which were a real surprise.

- 20% of the customers of the wholesale

business were profitable, contributing £300k.

Unfortunately the others pulled profitability

down to an overall loss of £100k. The only

viable option was to withdraw from certain

geographic regions because little could

be done to bring costs down to the levels

needed to turn this part of the business

round.

- 50% of the free trade made a healthy profit,

mainly because the product mix was

predominately 'draught'. Where the mix was

mainly 'bottled' this segment lost money.

- All tenanted and managed houses were

profitable, which was reassuring.

- Only 50% of the Take home/National business

was profitable. This segment needed working

on to build up gross margins.

The analyses in the model, showed management

where specific actions would lead to healthy

gains in profitability in the short to medium

term. Further refinement of the model then

delivered many pointers to subtle changes

in the business that helped it continue to build

a growing and robust bottom line.

Why did the project make such a difference to business performance?

This approach made all the difference. It uncovered where profits were being made or lost.

It showed the underlying reasons for losing money and what we needed to do to turn unprofitable business around.

And it gave management the confidence to drop whole segments of unprofitable business when there was no hope

of turning it to profit.

The company needed to understand its net margins for all its products and for all its customers.

browser implementation

For more information, contact: Managers-Net.